TABLE OF CONTENTS

Stripe vs PayPal vs Adyen: Payment Gateway Selection for Multi-Currency eCommerce

Payment processing is the only technology decision where every percentage point directly impacts your bottom line. Choose the wrong gateway, and you’re overpaying on every transaction, losing customers to payment failures, and struggling with international expansion.

For eCommerce directors and finance leaders at companies selling across multiple countries (US, UK, Australia, Canada, and beyond), the payment gateway decision involves complex trade-offs: transaction fees, authorization rates, supported payment methods, multi-currency capabilities, and settlement timing.

Three platforms dominate the conversation for multi-currency eCommerce: Stripe (developer favorite), PayPal (consumer brand recognition), and Adyen (enterprise powerhouse).

At Askan Technologies, we’ve integrated all three payment processors across 40+ eCommerce implementations processing $2M to $50M annually. These aren’t theoretical comparisons. We track authorization rates, actual transaction costs, dispute resolution efficiency, and currency conversion markups across real production systems.

The data reveals clear patterns: each platform excels in specific scenarios, but choosing based on brand recognition or developer preference costs tens of thousands annually in unnecessary fees and lost revenue from payment failures.

The Multi-Currency Payment Challenge

Before comparing platforms, let’s establish what multi-currency eCommerce actually requires.

Beyond Simple Currency Display

Many merchants think multi-currency just means showing prices in different currencies (£50 GBP instead of $65 USD). But true multi-currency commerce involves complex considerations:

Customer expectations per region:

US customers: Credit cards (Visa, Mastercard), digital wallets (Apple Pay, Google Pay), buy-now-pay-later (Affirm, Afterpay)

UK customers: Credit/debit cards, PayPal, digital wallets, bank transfers (faster payments)

Australia customers: Credit cards, PayPal, Afterpay (extremely popular), POLi (bank transfer)

EU customers: Credit cards, PayPal, SEPA direct debit, local methods (iDEAL in Netherlands, Sofort in Germany, Bancontact in Belgium)

Canada customers: Credit cards, digital wallets, Interac (debit network)

The complexity: Supporting one payment method is straightforward. Supporting 15+ payment methods across 5+ currencies while optimizing authorization rates and minimizing fees requires sophisticated gateway capabilities.

The Hidden Costs of Payment Processing

Transaction fees are just the beginning. Total payment cost includes:

| Cost Component | Typical Impact | Example at $10M Revenue |

| Base transaction fee | 2.5-3.5% | $250K-$350K |

| Currency conversion markup | 1-3% on FX | $30K-$90K |

| Failed authorization cost | Lost revenue | $200K-$400K |

| Dispute/chargeback fees | $15-$25 per dispute | $6K-$15K |

| Integration maintenance | Developer time | $12K-$24K |

| Total | $498K-$879K |

The difference between best and worst gateway choice: $200K to $400K annually at $10M revenue.

Stripe: The Developer’s Choice

Stripe launched in 2010 with a mission: make online payments simple for developers. That focus shows in every aspect of the platform.

Core Strengths

- Exceptional API Design

Stripe’s API is consistently rated the best in the industry. Clean, well-documented, predictable behavior.

Implementation speed:

- Basic integration: 2-3 days

- Advanced features (subscriptions, Connect): 1-2 weeks

- Multi-currency: Additional 1-2 days

- Comprehensive Payment Method Support

Available globally:

- Credit/debit cards (Visa, Mastercard, Amex, Discover)

- Digital wallets (Apple Pay, Google Pay, Microsoft Pay)

- Buy-now-pay-later (Klarna, Affirm, Afterpay/Clearpay)

Regional methods:

- Alipay, WeChat Pay (China)

- Bancontact, iDEAL, Sofort (Europe)

- SEPA Direct Debit (Europe)

- ACH Direct Debit (US)

- BECS Direct Debit (Australia)

Total: 135+ currencies, 50+ payment methods

- Strong Fraud Protection

Stripe Radar uses machine learning to detect fraud:

- Blocks 99.9% of fraudulent transactions

- False positive rate: Under 1%

- Customizable rules (block high-risk countries, velocity limits)

- No additional cost (included in transaction fees)

Real impact: A client processing $15M annually saw fraud losses drop from 0.8% ($120K) to 0.1% ($15K) after migrating to Stripe.

Pricing Structure

Standard pricing (most merchants):

- 2.9% + 30¢ per successful card charge (US)

- 3.4% + 30¢ per successful card charge (international cards)

- 0.8% additional for currency conversion

Volume pricing (negotiated above $1M/month):

- Starts around 2.5% + 20¢

- Can go as low as 2.2% at very high volumes

Example cost at $10M annual revenue:

| Transaction Type | Volume | Rate | Cost |

| US cards | $6M | 2.9% + 30¢ | $175,200 |

| International cards | $2M | 3.4% + 30¢ | $69,000 |

| Currency conversion | $2M | 0.8% | $16,000 |

| Total | $10M | $260,200 |

Effective rate: 2.6%

Stripe’s Multi-Currency Implementation

Stripe handles multi-currency in two ways:

Option 1: Presentment Currency

Charge customer in their local currency, receive settlement in your account currency. Stripe handles conversion with 1% markup.

Workflow:

- UK customer sees £100 price

- UK customer pays £100

- Stripe converts £100 to $130 USD (example rate)

- You receive $129 USD (after 1% conversion fee)

Option 2: Multi-Currency Accounts

Open separate Stripe accounts in different currencies. Receive direct settlement in local currency.

Workflow:

- UK customer sees £100 price

- UK customer pays £100

- You receive £100 directly in UK bank account

Best practice: Multi-currency accounts reduce conversion fees but require managing multiple bank accounts and currency exchange separately.

Where Stripe Struggles

Limited enterprise features: No advanced fraud management UI, basic reporting compared to Adyen, less sophisticated chargeback management.

Higher rates for high volume: At $50M+ annually, enterprise processors offer better rates.

Support quality: Email-based support can be slow for urgent payment issues (no dedicated account managers until very high volumes).

PayPal: The Trusted Brand

PayPal has 430+ million active accounts globally. That installed base makes PayPal a must-have for many merchants.

Core Strengths

- Consumer Trust and Recognition

Consumers trust PayPal. For first-time customers especially, seeing PayPal as a payment option increases conversion.

Data from our implementations:

| Customer Type | With PayPal | Without PayPal | Improvement |

| First-time visitors | 2.1% conversion | 1.6% conversion | +31% |

| Returning customers | 3.8% conversion | 3.7% conversion | +3% |

Impact: PayPal particularly helps with new customer acquisition.

- Buyer Protection Program

PayPal offers buyer protection (refunds if item not received or significantly different). This reduces purchase anxiety.

- One-Click Checkout

Customers with PayPal accounts can complete checkout in seconds without entering card details.

Average checkout time:

- Manual card entry: 90-120 seconds

- PayPal Express: 15-25 seconds

Abandonment rate:

- Manual checkout: 68%

- PayPal Express: 42%

Pricing Structure

Standard rates:

- 2.9% + 30¢ per transaction (US domestic)

- 4.4% + fixed fee (international transactions)

- 1.5% currency conversion fee

PayPal’s pricing complexity: Rates vary dramatically based on transaction type, countries involved, and payment method used.

Example scenarios:

| Scenario | Rate | Fee on $100 |

| US customer, US merchant | 2.9% + 30¢ | $3.20 |

| UK customer, US merchant | 4.4% + 30¢ | $4.70 |

| UK customer, UK merchant | 3.4% + 20p | £3.60 |

| Currency conversion (£ to $) | +1.5% | Additional $1.50 |

Total cost at $10M annual revenue (mixed international):

| Component | Cost |

| US domestic transactions (60%) | $192,000 |

| International transactions (40%) | $184,000 |

| Currency conversion | $60,000 |

| Total | $436,000 |

Effective rate: 4.36%

PayPal is significantly more expensive than Stripe for merchants with international sales.

PayPal’s Multi-Currency Approach

PayPal supports 200+ countries and 25 currencies through:

- PayPal Checkout: Customer pays in any supported currency. You receive settlement in your account currency.

- Multi-Currency Balance: Hold balances in multiple currencies. Useful if you have expenses in those currencies.

- PayPal Commerce Platform: More sophisticated integration with better reporting and webhooks (launched 2021, addressing past API limitations).

Where PayPal Struggles

High international fees: 4.4% on cross-border transactions is expensive compared to Stripe (3.4%) and Adyen (2.8%).

Account holds/freezes: PayPal is notorious for freezing merchant accounts during disputes, holding funds for weeks.

Poor developer experience: APIs historically weak (improving with Commerce Platform), webhook reliability issues, difficult error handling.

Chargeback bias: PayPal heavily favors buyers in disputes. Merchants often lose even with evidence.

Real story: A client had $45K frozen for 3 weeks during holiday season due to “suspicious activity” (sales spike from successful marketing campaign). Nearly destroyed their business.

Adyen: The Enterprise Platform

Adyen powers payments for Uber, Spotify, Microsoft, eBay, and hundreds of enterprise companies. It’s built for scale, complexity, and global operations.

Core Strengths

- Unified Platform

Adyen provides one integration for all channels:

- Online checkout

- Mobile apps (in-app payments)

- Point-of-sale (physical stores)

- Marketplaces (platform payments)

Why this matters: Unified reporting across all channels, consistent customer experience, simplified reconciliation.

- Superior Authorization Rates

Adyen’s platform optimizes authorization rates through:

- Smart routing (send transaction to best-performing acquirer)

- Network tokens (replace card numbers with tokens, higher approval rates)

- Local acquiring (process transactions locally in each market)

Real performance data (our implementations):

| Processor | Authorization Rate (US) | Authorization Rate (International) |

| Stripe | 96.2% | 93.8% |

| PayPal | 97.1% | 94.2% |

| Adyen | 97.8% | 96.4% |

Impact at $10M revenue:

Adyen’s 2.6% higher international authorization rate captures additional $52,000 in revenue (2.6% of $2M international sales) that would fail with Stripe.

- Transparent Interchange-Plus Pricing

Unlike Stripe/PayPal’s blended rates, Adyen charges:

- Actual interchange fees (what Visa/Mastercard charge)

- Plus fixed markup (your margin to Adyen)

Example:

- Visa interchange: 1.65% + 10¢

- Adyen markup: 0.60% + 5¢

- Total: 2.25% + 15¢

Advantage: Predictable costs, lower rates for merchants processing $5M+

- Advanced Reporting and Analytics

Adyen’s dashboard provides:

- Authorization rate by card type, country, time of day

- Decline reason analysis (expired cards, insufficient funds, fraud)

- Settlement reconciliation across currencies

- Revenue optimization recommendations

Pricing Structure

Interchange-plus model:

- Interchange: 1.5-2.5% (varies by card type)

- Adyen markup: 0.6% + €0.10 (negotiable at volume)

- Typical total: 2.1-3.1%

Monthly minimums: €120 to €500 depending on contract

Example cost at $10M annual revenue:

| Component | Cost |

| Interchange fees | $190,000 |

| Adyen markup (0.6%) | $60,000 |

| Per-transaction fees | $12,000 |

| Monthly minimum | $3,000 |

| Total | $265,000 |

Effective rate: 2.65%

Adyen costs similar to Stripe at $10M volume, but offers better authorization rates and enterprise features.

Adyen’s Multi-Currency Excellence

Adyen excels at international commerce through:

- Local Acquiring: Process transactions in-country (better authorization rates, lower fees).

- Dynamic Currency Conversion (DCC): Let customers pay in their home currency while you receive your settlement currency.

- Multi-Currency Settlement: Receive payouts in 30+ currencies.

- 250+ Payment Methods: Extensive local payment method support (Alipay, WeChat, iDEAL, Swish, MobilePay, Pix, etc.).

Where Adyen Struggles

High barrier to entry: Minimum volumes typically $2M-$5M annually. Below this, they may decline or charge higher rates.

Complex setup: Integration takes 4-8 weeks (vs 2-3 days for Stripe). Requires technical sophistication.

Steeper learning curve: More complex than Stripe. Documentation good but assumes higher technical knowledge.

Not cost-effective for small businesses: Monthly minimums and platform complexity make Adyen overkill for businesses under $5M revenue.

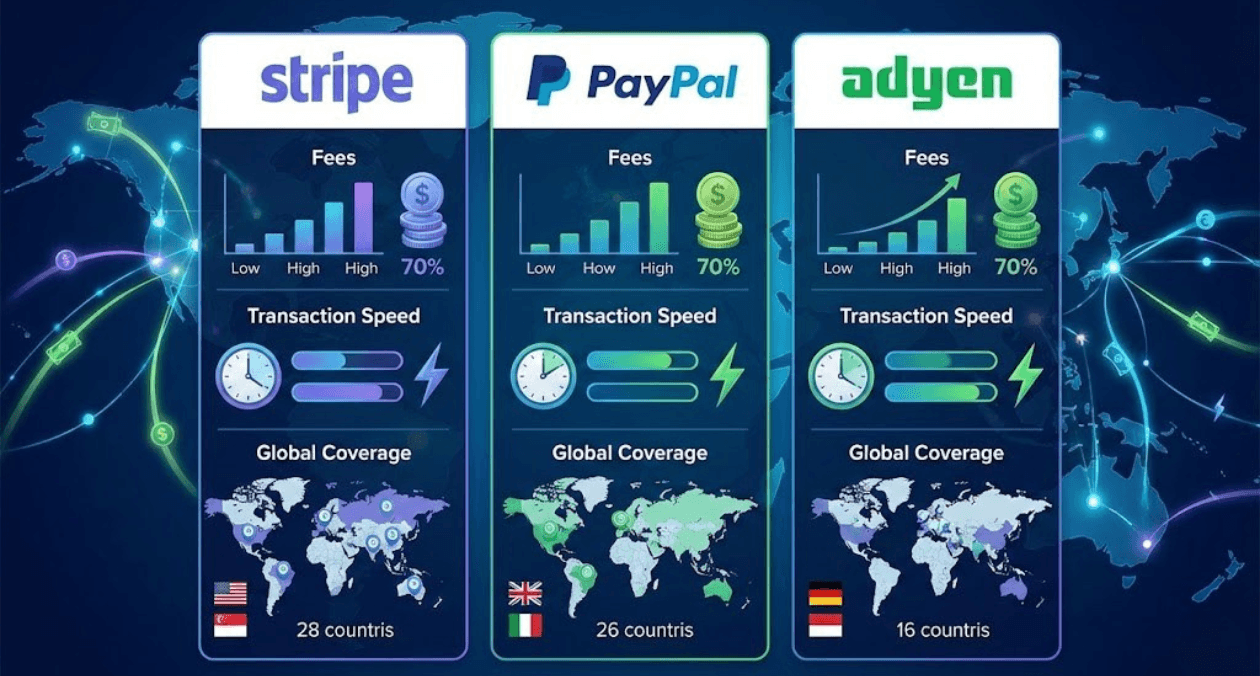

Head-to-Head Comparison

Transaction Costs (at $10M annual revenue)

| Gateway | US Domestic | International | Currency Conversion | Total Annual Cost |

| Stripe | 2.9% + 30¢ | 3.4% + 30¢ | 1% | $260K |

| PayPal | 2.9% + 30¢ | 4.4% + 30¢ | 1.5% | $436K |

| Adyen | 2.2% + 15¢ | 2.8% + 15¢ | 0.6% | $265K |

Savings over PayPal:

- Stripe saves: $176K annually (40% reduction)

- Adyen saves: $171K annually (39% reduction)

Payment Method Coverage

| Region | Stripe | PayPal | Adyen |

| Credit/Debit Cards | ✅ Excellent | ✅ Excellent | ✅ Excellent |

| Digital Wallets | ✅ Apple/Google Pay | ✅ PayPal + others | ✅ All major wallets |

| Buy-Now-Pay-Later | ✅ Good (Klarna, Affirm) | ✅ PayPal Pay Later | ✅ Excellent (all providers) |

| Local Payment Methods | ⚠️ Growing | ⚠️ Limited | ✅ 250+ methods |

| Bank Transfers | ✅ ACH, SEPA | ⚠️ Limited | ✅ Extensive |

Winner for method coverage: Adyen

Authorization Rates

| Gateway | US Cards | International Cards | Revenue Lost to Failures |

| Stripe | 96.2% | 93.8% | $100K (at $10M) |

| PayPal | 97.1% | 94.2% | $80K |

| Adyen | 97.8% | 96.4% | $48K |

Winner for authorization: Adyen (saves $52K in recovered revenue vs Stripe)

Developer Experience

| Feature | Stripe | PayPal | Adyen |

| API quality | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ |

| Documentation | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ |

| Integration speed | 2-3 days | 1-2 days | 4-8 weeks |

| Testing tools | Excellent | Good | Excellent |

| SDKs/Libraries | 15+ languages | 10+ languages | 12+ languages |

Winner for developers: Stripe

Decision Framework

Choose Stripe If:

- You’re processing under $5M annually

- Developer experience and speed to market are priorities

- You need flexibility to start small and scale

- You want excellent documentation and community support

- You’re selling primarily in US, UK, EU, Australia

Ideal customer: Growing eCommerce companies, SaaS businesses, digital product sellers

Choose PayPal If:

PayPal brand recognition significantly increases your conversion

- You’re selling primarily to consumers (not B2B)

- You’re processing mostly domestic transactions

- Your average order value is under $50 (PayPal’s fixed fees matter less)

- You want to offer PayPal Credit/Pay Later financing

Ideal customer: Consumer-focused businesses, marketplaces, businesses targeting PayPal’s 430M users

Choose Adyen If:

You’re processing $5M+ annually

- International sales are significant (30%+ of revenue)

- Authorization rate improvements justify complexity

- You need omnichannel (online + mobile + in-store)

- You want enterprise-grade reporting and support

- You’re expanding to markets with local payment methods

Ideal customer: Enterprise eCommerce, global retailers, omnichannel brands, marketplaces

The Hybrid Strategy

Many successful merchants use multiple processors strategically:

Primary processor (80% of volume): Stripe or Adyen

Secondary processor (20% of volume): PayPal

Why this works:

- Offer PayPal for customers who prefer it (captures PayPal-only shoppers)

- Use Stripe/Adyen for card payments (better rates, better control)

- Redundancy (if one processor has issues, the other continues working)

Implementation: Payment orchestration layer routes transactions to optimal processor based on payment method, customer location, and cost.

Key Takeaways

- Stripe best for growing businesses under $5M revenue (excellent developer experience, fair pricing, comprehensive features)

- PayPal essential for consumer trust but expensive for international (use alongside Stripe/Adyen, not as sole processor)

- Adyen wins for enterprises processing $5M+ with international sales (best authorization rates, lowest costs at scale)

- Payment costs vary 40-60% between best and worst gateway choice ($260K vs $436K at $10M revenue)

- Authorization rates matter more than fees for some businesses (1% authorization improvement = $100K recovered revenue)

- Multi-currency requires local payment methods not just currency display (iDEAL in Netherlands, Afterpay in Australia)

- Hybrid strategy captures best of all platforms (use multiple processors for different payment methods)

How Askan Technologies Optimizes Payment Processing

As an ISO-9001 certified development partner, we’ve integrated Stripe, PayPal, and Adyen across 40+ eCommerce implementations processing $2M to $50M annually.

Our Payment Integration Services:

- Gateway Selection Consulting: Analyze transaction patterns and recommend optimal processor(s)

- Multi-Gateway Implementation: Integrate multiple processors with smart routing

- Payment Optimization: A/B test payment flows, optimize authorization rates

- Multi-Currency Setup: Configure currency presentation, settlement, and tax calculation

- PCI Compliance: Ensure secure payment handling meeting all requirements

Recent Payment Implementations:

- Fashion retailer: Hybrid Stripe + PayPal setup, $8K monthly savings vs PayPal-only

- Electronics store: Adyen integration, 2.3% authorization rate improvement = $180K recovered revenue

- B2B platform: Stripe with ACH, reduced payment processing costs 48%

We deliver payment solutions with our 98% on-time delivery rate and 30-day free support guarantee.

Final Thoughts

Payment gateway selection isn’t about choosing the most popular brand. It’s about matching processor capabilities to your business model, transaction patterns, and growth trajectory.

Stripe wins for speed, flexibility, and developer experience. PayPal wins for consumer trust and brand recognition. Adyen wins for international scale and enterprise sophistication.

The companies optimizing payment costs in 2026 are those that chose strategically based on data, not defaults. They understand that every percentage point in fees or authorization rates compounds across millions in transactions.

Start by analyzing your current costs. Model scenarios with each processor. Consider hybrid strategies. Test authorization rates in production with small percentage routing.

Your payment gateway isn’t just a technical integration. It’s a direct line to your revenue and margins. Optimize it accordingly.

Most popular pages

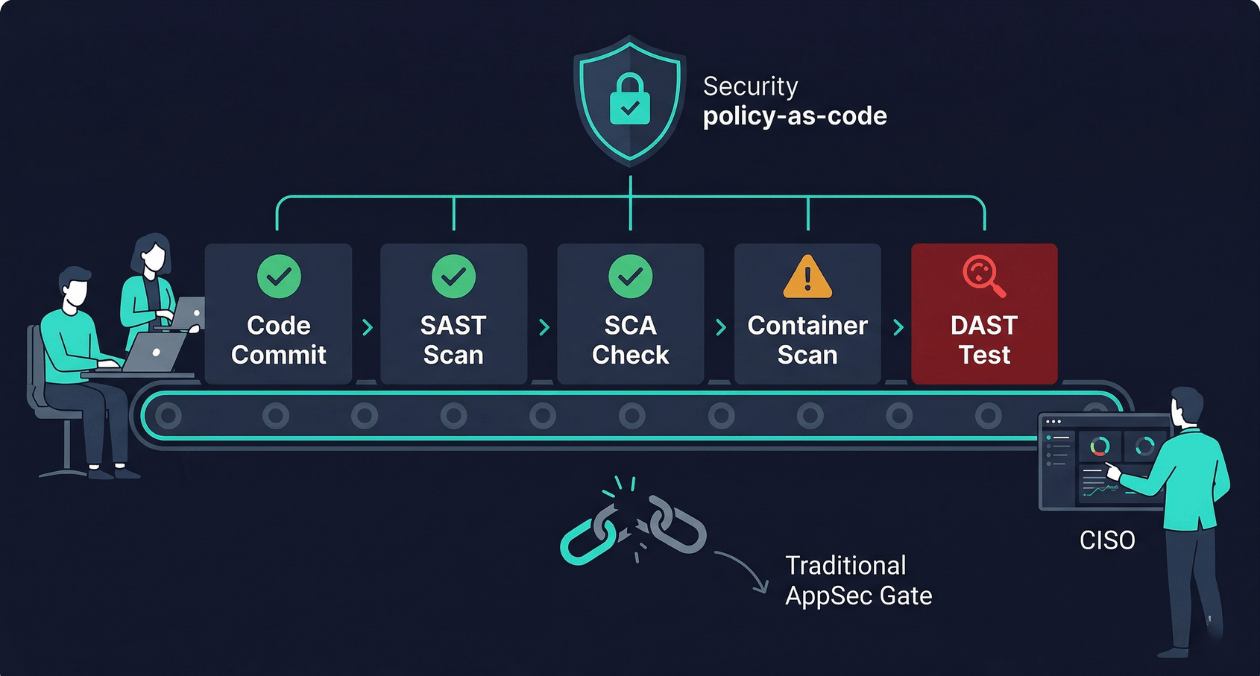

Security as Code: Embedding AppSec Into CI/CD Without Slowing Releases

There is a particular kind of friction that security teams and engineering teams share without ever quite resolving. Engineering wants to ship fast. Security...

-

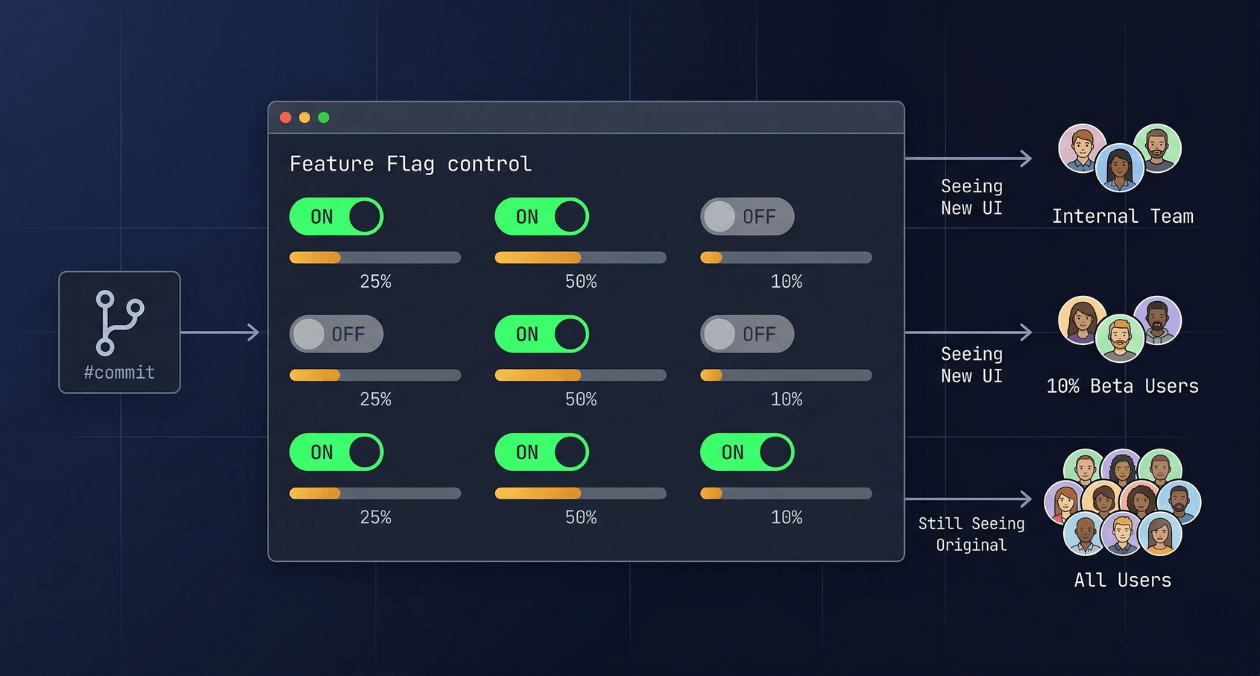

Feature Flags in Production: Progressive Delivery Without the Risk

The deploy button used to mean something definitive. You shipped code, users got the new version, and if something broke you scrambled to roll...

-

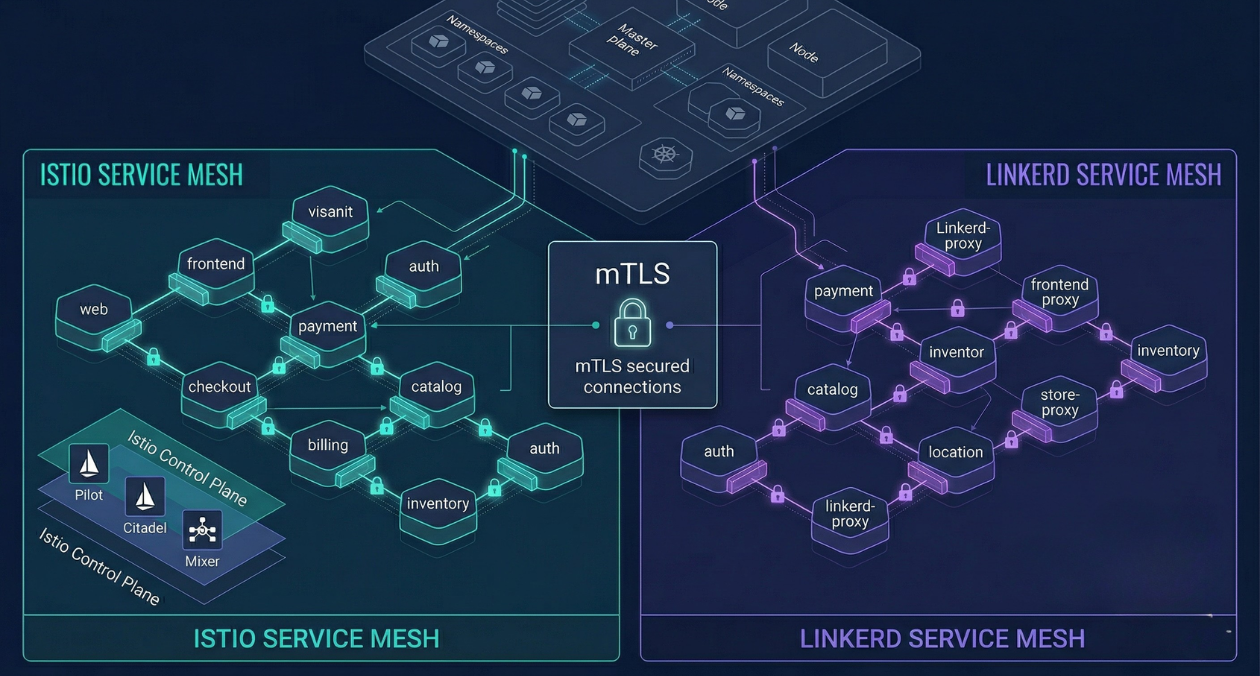

Service Mesh Architecture: When Istio and Linkerd Are Worth the Complexity

There is a specific moment in the growth of a microservices platform when the operational questions start arriving faster than the answers. How do...

Security as Code: Embedding AppSec Into CI/CD Without Slowing Releases

There is a particular kind of friction that security teams and engineering teams share without ever quite resolving. Engineering wants to ship fast. Security...

Feature Flags in Production: Progressive Delivery Without the Risk

The deploy button used to mean something definitive. You shipped code, users got the new version, and if something broke you scrambled to roll...

Service Mesh Architecture: When Istio and Linkerd Are Worth the Complexity

There is a specific moment in the growth of a microservices platform when the operational questions start arriving faster than the answers. How do...